Freqtrade: Awesome oscillator has a lot of missing values

Step 1: Have you search for this issue before posting it?

Yes

Step 2: Describe your environment

- Python Version: 3.6.8

- CCXT version: 1.18.551

- Branch: Develop

- Last Commit ID: 3e2c808b4bef4984a1f129e67736f18df327ab92

Step 3: Describe the problem:

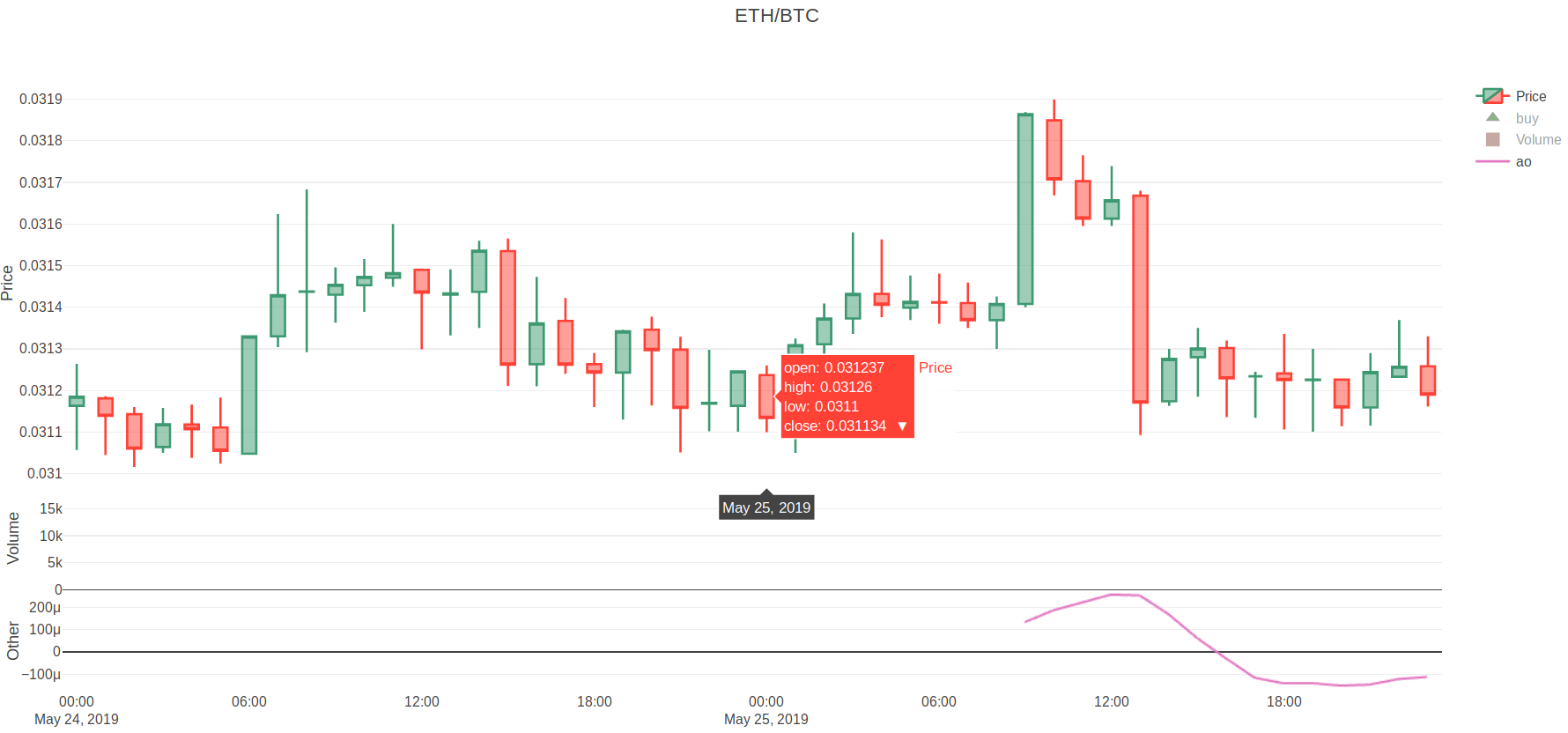

I created custom strategy with only one indicator - qtpylib.awesome_oscillator. After that I ran:

python3 ./scripts/plot_dataframe.py -s CustomStrategy -p ETH/BTC --indicators2 ao --timerange 20190524-20190526

and opened user_data/freqtrade-plot.html.

Observed Results:

The awesome oscillator on freqtrade-plot has a lot of missing values(but of course tradingview.com has them). I get this issue for all pairs, and I just can't buy due to this.

konstantin-doncov

konstantin-doncov

All 4 comments

awesome oscillator in qtpy uses the exponential weighted function with default length of 34:

def awesome_oscillator(df, weighted=False, fast=5, slow=34)

That's what you see on the graph: first value is printed after 34 starting candles. These are not 'missing' values, it's a starting period for calculation of the first value of the mean function. If you have used EMA(100) in the strategy, you would get first value of EMA only after 100 starting candles.

Your time range is just 2 days, i.e. only 48 1h-candles. Try to use a longer time range.

hroff-1902

on 29 May 2019

hroff-1902

on 29 May 2019

In addition to the above:

Tradingview has the full length of the indicator because it has data from before what you see - however you should be able to archive this as follows:

You could also run backtesting seperately (with a longer timerange) by using --export trades --export-filename user_data/backtest_export.json and then plot a smaller timerange (not at the beginning of the backtest period) to avoid this problem (don't forget to add --export-filename user_data/backtest_export.json to the plot-script so it's using the exported trades.

xmatthias

on 29 May 2019

xmatthias

on 29 May 2019

@xmatthias "with a longer timerange" 😎

Thanks for example of partial plotting of the results, I did not think of such a use case.

This probably should be fixed somewhere in the docs in a section like "Efficient usage of freqtrade and its tools".

hroff-1902

on 29 May 2019

Many thanks for the explanation! Also, I have another question, more related to the ta-lib, but I think you can help me with it too:

https://github.com/mrjbq7/ta-lib/issues/266

konstantin-doncov

on 30 May 2019

Related issues

Mesengeros

·

4Comments

Mesengeros

·

4Comments

Axel-CH

·

3Comments

Axel-CH

·

3Comments

cgw-9527

·

3Comments

cgw-9527

·

3Comments

yperfanov

·

4Comments

yperfanov

·

4Comments

Dante2333

·

4Comments

Dante2333

·

4Comments

Most helpful comment

In addition to the above:

Tradingview has the full length of the indicator because it has data from before what you see - however you should be able to archive this as follows:

You could also run backtesting seperately (with a longer timerange) by using

--export trades --export-filename user_data/backtest_export.jsonand then plot a smaller timerange (not at the beginning of the backtest period) to avoid this problem (don't forget to add--export-filename user_data/backtest_export.jsonto the plot-script so it's using the exported trades.